CSRD Reporting Considerations

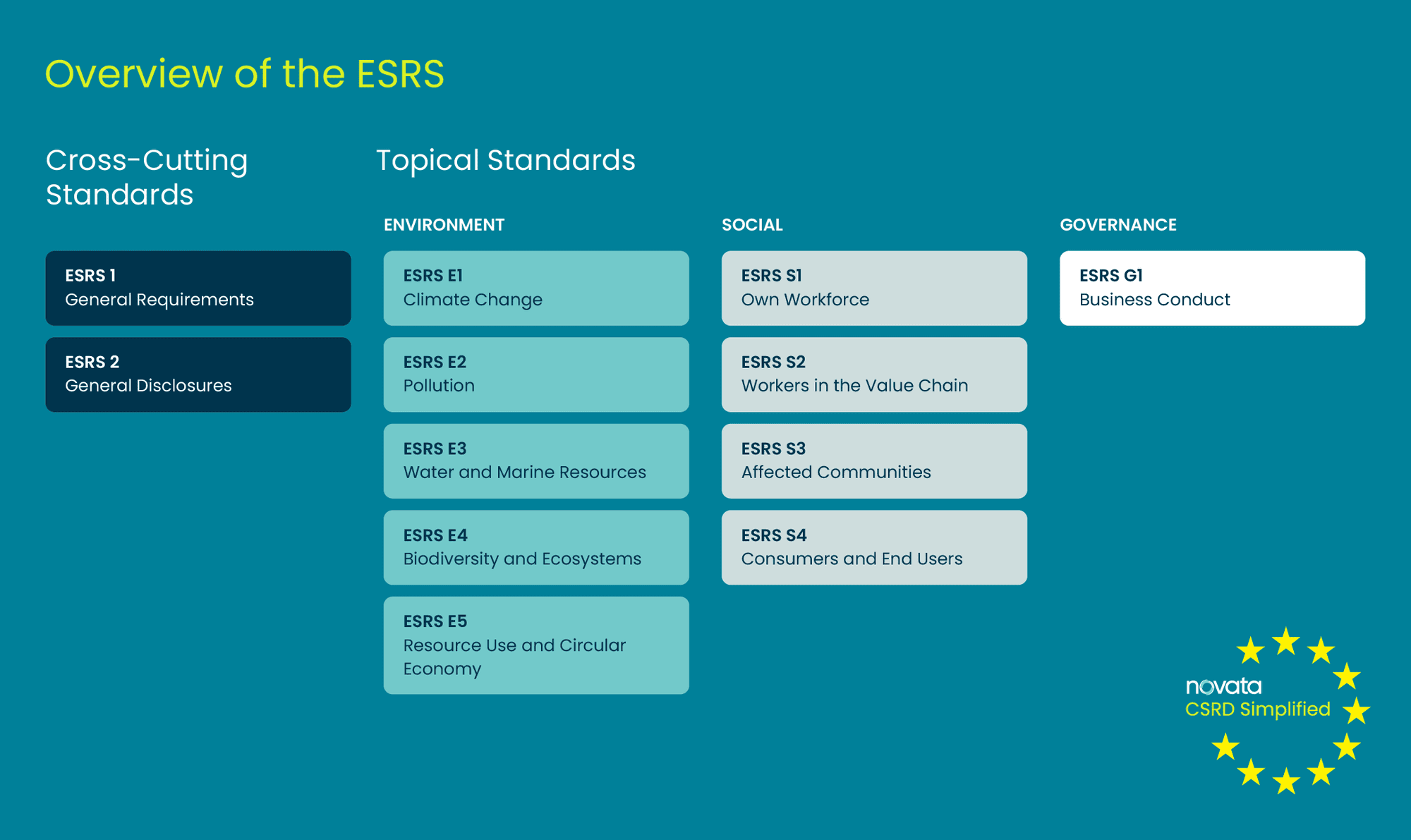

To specify the reporting requirements, the EU has introduced the European Sustainability Reporting Standards (ESRS). Currently, there are two overarching ESRS standards (ESRS 1 and 2) and 10 topic-specific standards, with additional sector-specific standards scheduled for adoption in 2026.

While all companies must adhere to the reporting requirements in ESRS 1 and 2, the 10 topic-specific standards require companies to report only on information that is relevant to their business and value chain.

To determine what is material, companies must apply a double-materiality perspective. This approach considers both the impact the company has on the environment and society (impact materiality) and the actual or potential impact that sustainability issues may have on the business itself (financial materiality).

To assess this, companies will be conducting what is called a double materiality assessment. The double materiality assessment process will ask companies to draw up an initial list of potential impacts, risks and opportunities (IROs). Doing so, companies might leverage existing resources such as:

Climate risk assessments

Risk management documents

Internal policies

Peer research and ESG reports

Past materiality assessments

Due diligence processes

The initial list of IROs will be assessed for materiality. As part of this process, it’s advised that companies engage with stakeholders such as customers, suppliers, investors, and affected communities. During the stakeholder engagement process, new IROs may also resurface, which will need to be assessed for materiality.

IN BRIEF

Impact materiality refers to a company's impact on people or the environment. This includes actual or potential impacts, as well as a company's impact through its upstream and downstream value chain.

Financial materiality refers to the effects of sustainability matters on a company's cash flows, financial performance, access to finance or cost of capital in the short-, medium- and long-term. See EFRAG's Implementation Guidance 1 for more information.

All IROs must be assessed for materiality from both an impact and a financial perspective. However, a topic is considered material if it is significant from either perspective. Additionally, the regulation mandates that companies evaluate materiality across short-, medium-, and long-term timeframes.

Materiality assessments consider factors such as the scale, scope, irreversibility, and likelihood of the IRO. Depending on whether the IRO represents an impact, risk, or opportunity—and whether it is actual or potential—different dimensions of materiality must be evaluated. For instance, actual negative impacts are assessed based on their scale, scope, and irreversibility, while potential impacts must also consider the likelihood of occurrence.

In conducting these assessments, companies will need to set thresholds that align with their specific business contexts. For example, a large multinational may establish a higher threshold for scale compared to a smaller company serving local markets.

01 Understand the Context An essential part of the double materiality assessment is understanding the context. This includes:

Gaining insight into your company’s activities and business relationships, including products, services, and the geographic locations of your operations.

Understanding your stakeholders and interactions with them across the entire value chain.

Analysing media coverage, industry peers, sector-specific benchmarks, and sustainability trends.

Understanding the legal and regulatory environment, particularly sustainability-related regulations.

This contextual information is essential for the double materiality assessment (DMA) and will shape the IROs you identify, as well as the stakeholders you engage with. Additionally, this context must be reported as part of the mandatory disclosures. Getting a head start on gathering this information will help ensure a solid foundation for your DMA.

02 Obtain Stakeholder Buy-InThe double materiality assessment (DMA) is inherently a cross-functional effort that requires active involvement and support from a broad range of stakeholders across the organisation. Building understanding and commitment from all key stakeholders is essential to ensure the success of the process.

As part of this effort, educating stakeholders across the business on CSRD requirements early on will support a smoother, more successful implementation.

03 Consider Diverse InsightsUse a range of data sources to identify and evaluate IROs, such as recognised frameworks, industry benchmarks, stakeholder interviews, focus groups, or surveys. Many valuable resources may already exist within your business; consider compiling notes from recent board discussions, reviewing risks identified in policies, analysing supplier audits, and examining recent materiality assessments.

Remember to assess company-specific impacts, risks, and opportunities not explicitly mentioned in the ESRS, as they must also be evaluated for materiality—and reported if deemed material. Leveraging various methods to gather this information will foster deeper engagement and provide richer insights.

04 Collaborate When assessing financial materiality, engage representatives from risk, finance, and legal divisions. They will be able to assess the financial implications of sustainability risks and will potentially have dealt with them in the past.

Some topics will be new to these business functions, so provide educational resources to support their understanding and application of financial materiality to ESG topics. Cross-functional collaboration will also create synergies for the business and ensure CSRD can function as a catalyst for business transformation.

05 Validate Once impact and financial materiality assessments are complete, validate these with stakeholders, particularly senior leadership, who should sign off on the assessment.

06 Be Transparent and Stay Up-to-DateBe transparent about the assessment process and engage with stakeholders throughout. As a best practice, update the assessment regularly to reflect changes to your business landscape as well as the dynamic nature of social and environmental changes. Rather than a one-off exercise, double materiality and CSRD should be seen as a continuous process.

Less than €10,000

€10,000-€50,000

More than €50,0000

The double materiality assessment is a cross-functional effort that requires support from a broad range of stakeholders.

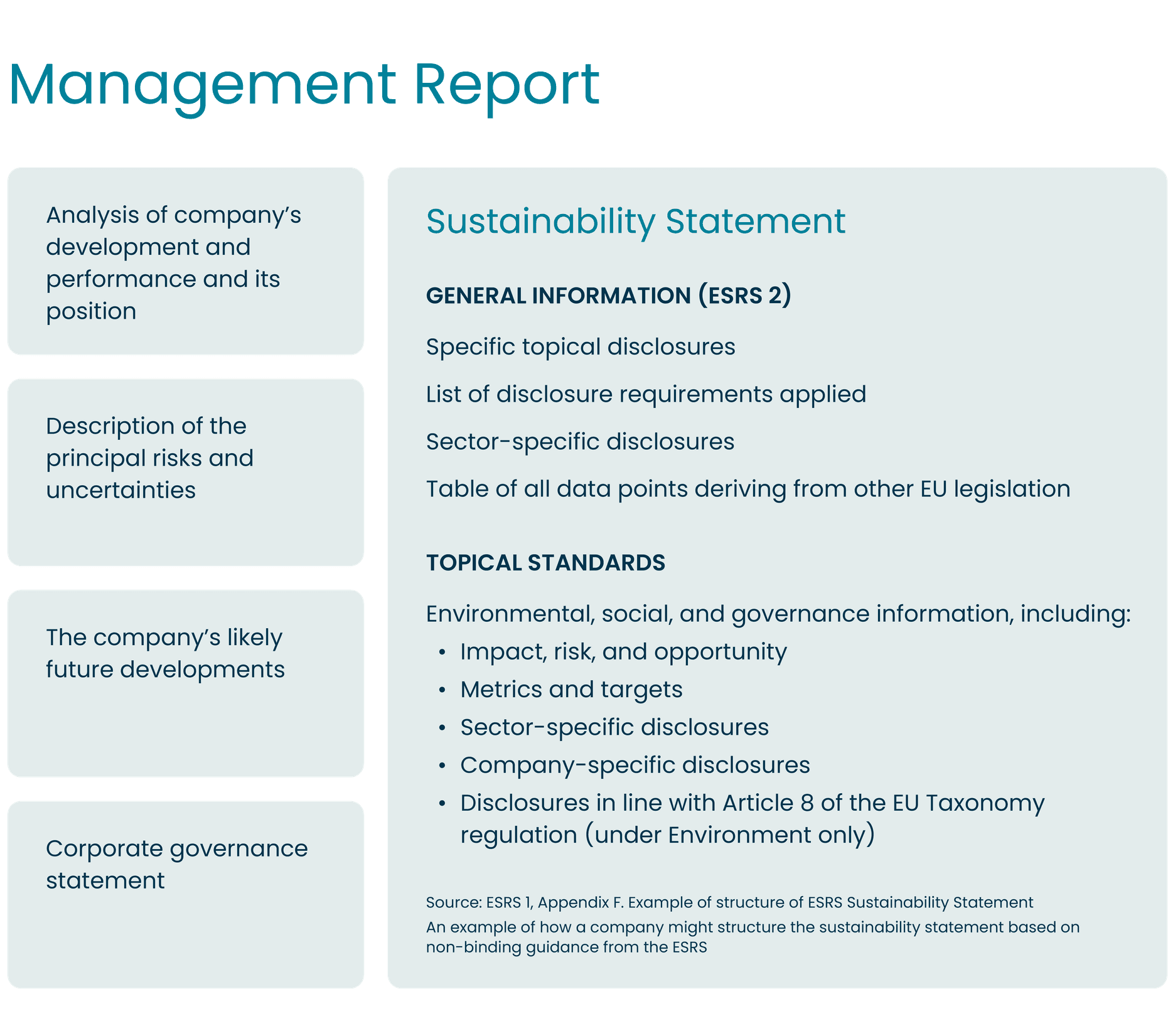

Following the double materiality assessment, companies need to ensure they have the data, processes, and expertise to report on ESG topics. The European Sustainability Reporting Standards (ESRS) are based on draft standards developed by EFRAG to support CSRD implementation. The ESRS guide the “how” and the “what” and act as the reporting framework companies must use to disclose their sustainability performance under the CSRD.

The ESRS set out two cross-cutting standards which apply to all sustainability matters and provide general reporting concepts with overarching disclosure requirements and data points. Ten topical standards for the disclosure of ESG information are also provided. Together, all 12 standards push companies to disclose quantitative and qualitative metrics and targets, details on their governance and strategy to address material sustainability topics, and information regarding the impacts, risks, and opportunities arising from those topics.

Annex I sets out the 12 ESRS and Annex II provides a list of acronyms and a glossary of terms. The ESRS requires qualitative and quantitative information to be:

Relevant. Information can affect the decisions of any key stakeholders.

Faithfully Represented. Information must be complete, neutral, and accurate.

Comparable. Information can be compared with information provided by the company in previous periods, but also with information provided by other companies.

Verifiable. Give users confidence that information is complete, neutral, and accurate.

Understandable. Reasonable, knowledgeable users must be able to readily comprehend the information. It should be clear and concise.

Spotlight on Data in the ESRSThe ESRS include 85 disclosure requirements and over 1000 data points. This is a lot of data to collect and manage and will require a robust data management system that also allows independent third-party assurance to run smoothly.

The easiest way to think about the CSRD and the ESRS is that the CSRD is the regulation while the ESRS are the instructions for how to adhere to the regulation.

To give companies, especially smaller companies, more time collect and report data, the first set of standards introduces relief measures for one, two, and three years. These include:

01 In the first year of reporting, all companies, regardless of size, have the option to opt out of disclosing the expected financial impacts of risks from environmental issues.

02Companies can choose to only provide qualitative disclosures on these financial impacts for the subsequent two years.

03Companies are also not required to report on certain workplace disclosures in the first year of reporting. These include metrics related to social protection, people with disabilities, and work-life balance.

Disclosure of Scope 3 greenhouse gas emissions (ESRS E1) and other disclosures on their own workforce (ESRS S1) in the first reporting year

Disclosures on biodiversity (ESRS E4), workers in the value chain (ESRS S2), affected communities (ESRS S3), and consumers (ESRS S4) in the first two reporting years

However, the ESRS do not consider situations where the absence of data would justify omitting the disclosure of material information.

01 Enhanced TransparencyWhile the CSRD doesn’t mandate new targets or policies, companies must disclose detailed information about their sustainability efforts, including policies, action plans, and governance structures. This also involves how sustainability KPIs impact executive pay and Board incentives, increasing visibility and accountability.

02 Confidence in Data ProcessesReports must be certified by an accredited auditor, including for non-European companies. This means businesses must ensure their data processes and assessments are robust and reliable before disclosure. On top of assuring the reported datapoints, the DMA too needs to be assured.

03 Climate Impact Disclosures and Transition Plans The CSRD requires companies to assess the potential impacts of climate change on their business models and financial health through climate scenario analysis. Even if a company deems climate change non-material, they must justify that decision. Additionally, by 2027, large companies will need to present a climate transition plan aligned with the Paris Agreement, making the CSRD more ambitious than similar regulations around the world.

The Sustainability Statement must follow a specific format and be included in the management report, alongside financial statements. It must be digitally tagged in the European Single Electronic Format (ESEF) for easy accessibility1 and analysis, covering general, environmental, social, and governance information.

1 The final draft of the ESRS XBRL Taxonomy was published in August 2024, and is currently being submitted to the European Commission and the European Securities and Markets Authority (ESMA) for approval. Digital tagging of ESRS will not be mandatory for companies until the EC adopts the XBRL taxonomy as part of the ESEF RTS that will be prepared by ESMA. It's likely that it will first be used in 2026 for Fiscal Year 2025 reports.