Understanding the CSRD

In today’s rapidly evolving business landscape, regulatory bodies, consumers, and investors alike are demanding greater transparency and accountability from companies regarding their environmental and social impact. Against this backdrop, the Corporate Sustainability Reporting Directive (CSRD) is a groundbreaking regulatory framework poised to reshape the way companies approach sustainability reporting.

For companies across Europe and beyond, the CSRD represents a fundamental change in how business performance is measured, taking into account not only financial outcomes but also how companies manage their environmental, social, and governance (ESG) risks and opportunities. But what does this mean for businesses, and why should companies care?

The CSRD is a legally binding European directive, and its broad scope includes more than 50,000 companies within and outside the EU. Failure to comply may lead to both penalties and reputational harm. In practice, these penalties are determined by individual EU member states and integrated into their national laws. As a result, the penalties companies face can differ across countries. Beyond avoiding penalties, compliance offers a powerful way for companies to align with investor expectations, stay ahead of competitors, and enhance risk management.

The data collected through CSRD compliance can provide valuable insights on a company’s risk management and sustainability practices, ultimately improving transparency. Investors may also gauge how companies are integrating macro-trends such as planning for climate change into business strategy, which may enhance investor confidence.

Introduced by the European Commission, the Corporate Sustainability Reporting Directive (CSRD), requires companies in scope of the regulation to report on the impacts, risks, and opportunities arising from social, environmental, and governance issues.

The CSRD aims to help key stakeholders, such as investors, lenders, business partners, and consumers, better evaluate the sustainability performance of companies. It is part of the European Union’s broader plan to direct capital flows towards sustainable investment and aims to elevate the importance of sustainability reporting in investment decision-making.

As a crucial part of the European Green Deal, the CSRD plays a role in connecting other EU regulations, such as the EU Taxonomy and the Sustainable Finance Disclosure Regulation (SFDR).

Like the SFDR, the CSRD pushes for increased transparency of sustainability matters and a standardised format for reporting sustainability matters. The aim is to improve transparency and increase data availability for investors who rely on the information to fulfill their disclosure requirements. If successful, this regulation will undoubtedly ease the challenges many investors have faced when assessing the financial risks and opportunities associated with existing and target investee companies.

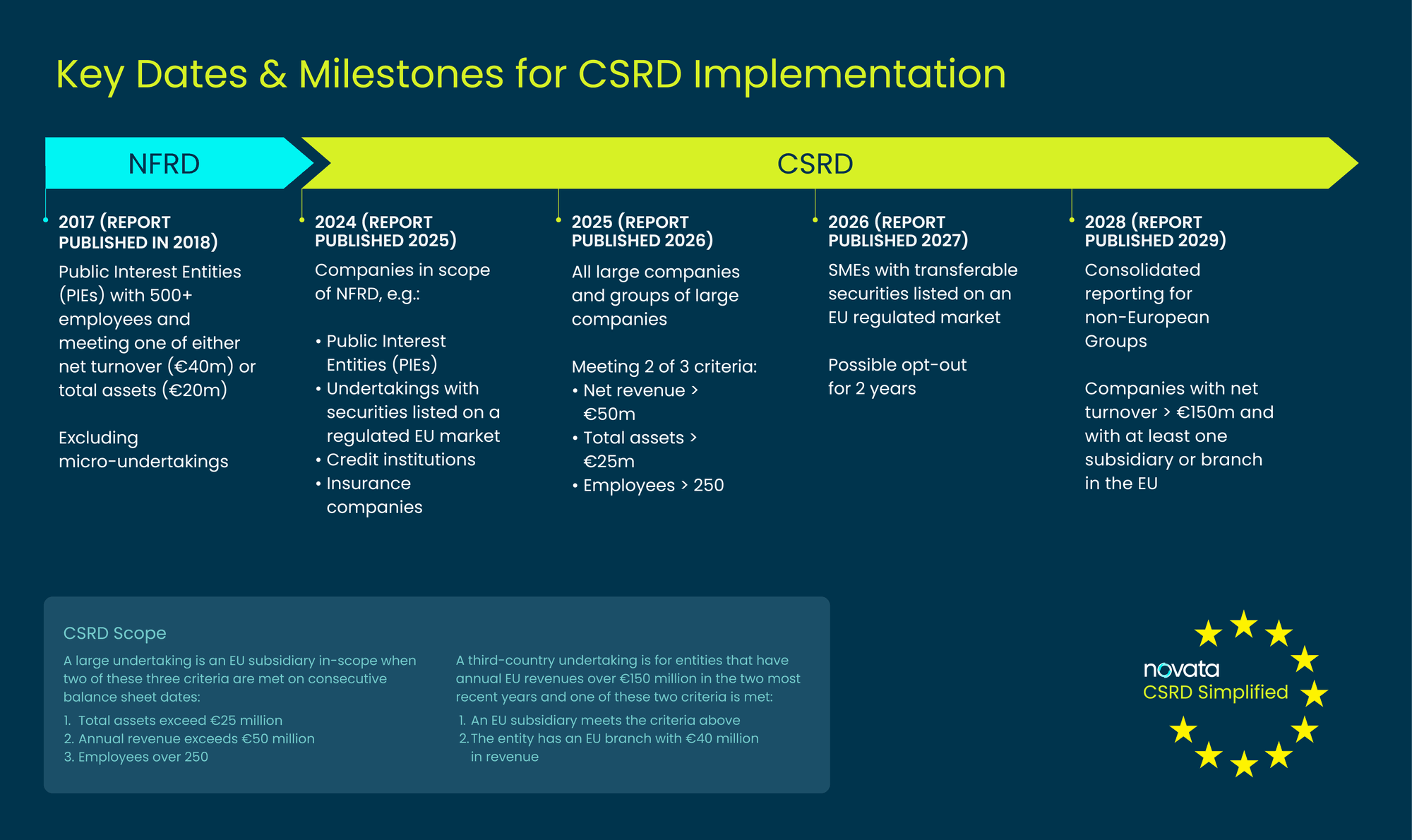

Notably, the CSRD amends and broadens the reporting requirements of its precursor, the Non-Financial Reporting Directive (NFRD), which remains in force until companies in scope of CSRD have to apply the new rules.

More than 50,000 companies in the EU and 10,400 non-EU companies will be affected by the CSRD, according to European Commission estimates.

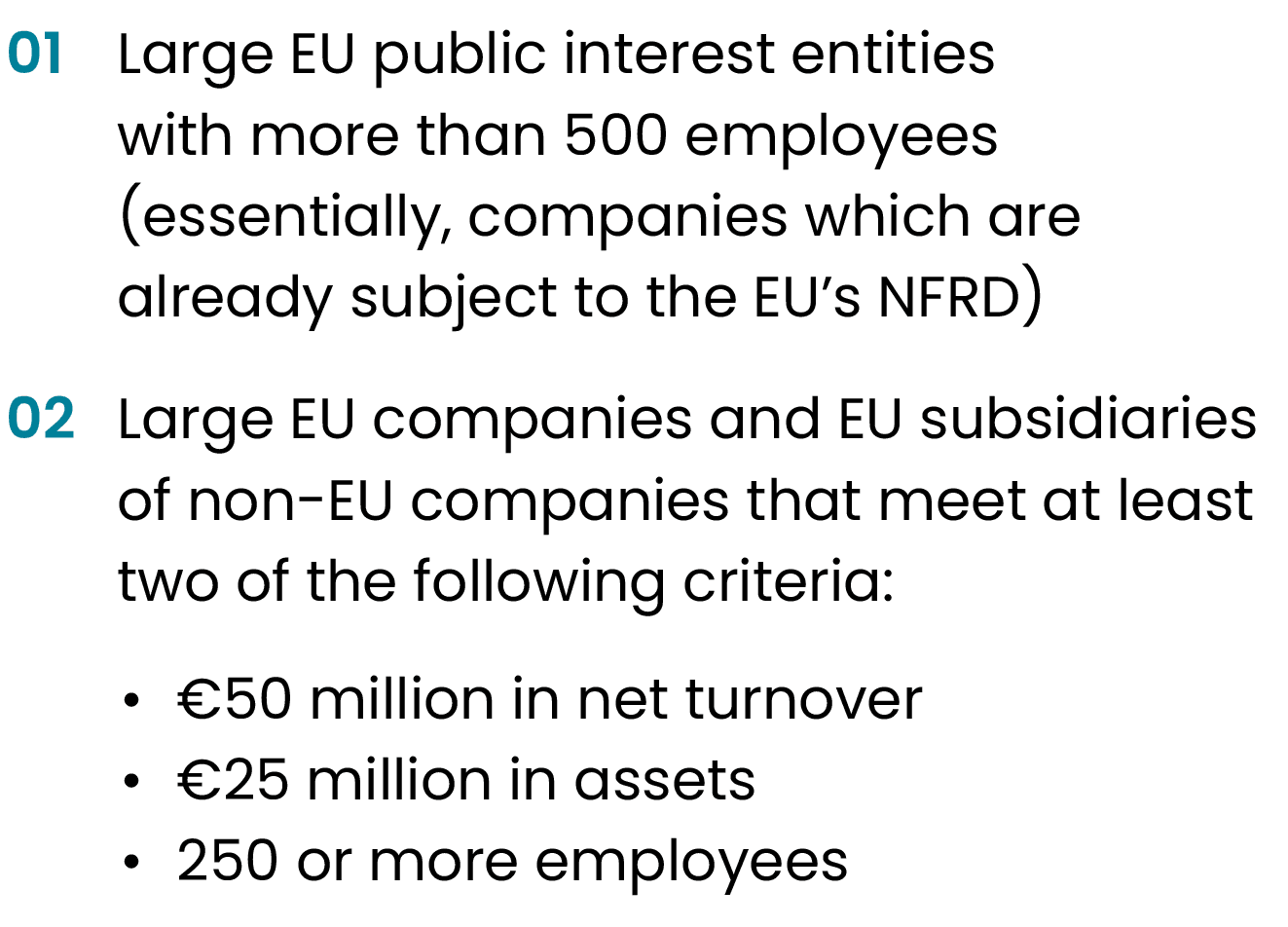

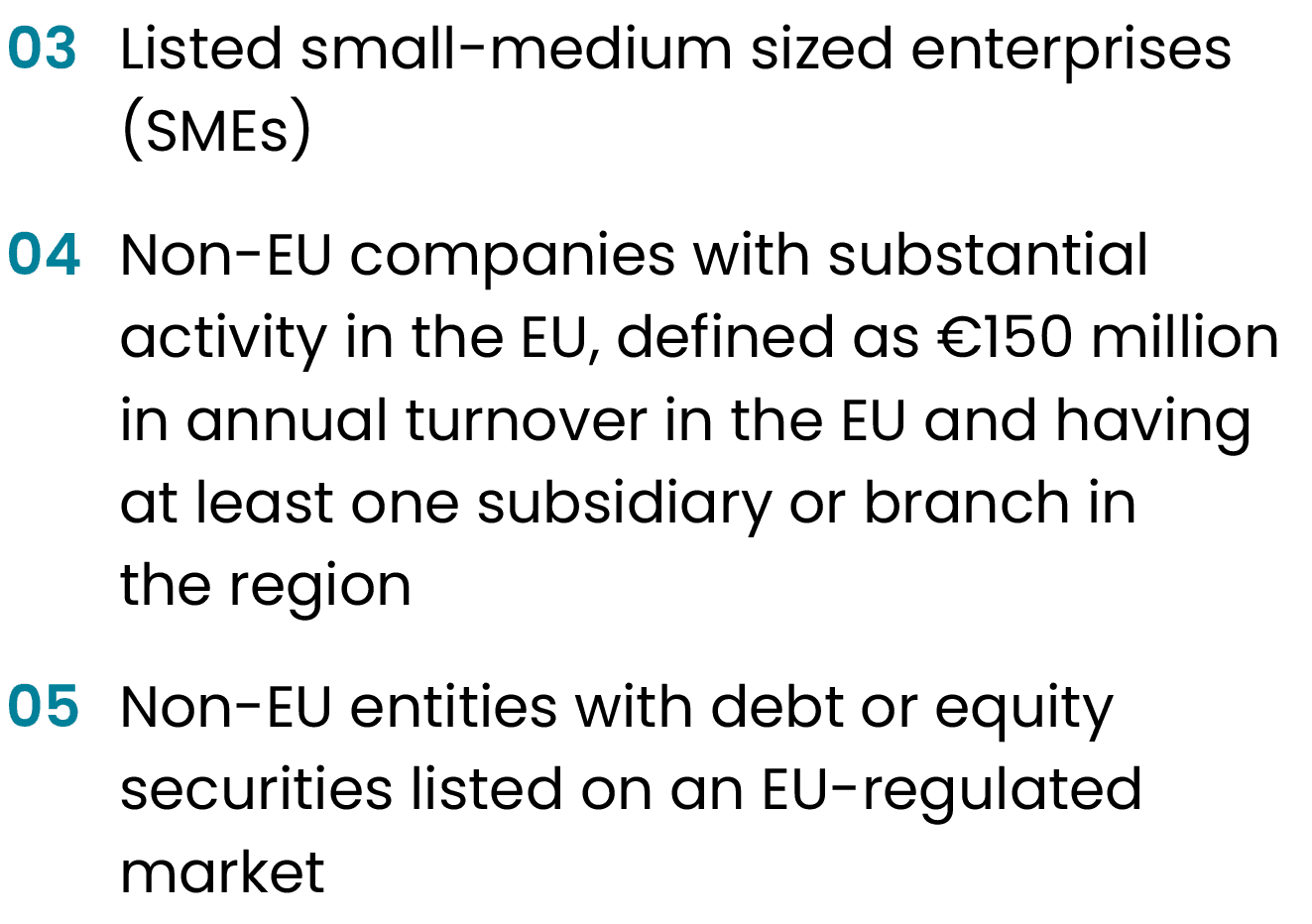

Article 5 of the CSRD outlines the applicability of the regulation for different types of entities. The breakdown includes:

The CSRD is adopting an iterative approach to reporting, with more companies falling into scope each year. The first group of companies began collecting data in 2024 (to report in 2025), with others following each year after.

Download the Report

The European Commission recognises that companies may need time to set up processes and controls for collecting this data. Therefore, it has included a three-year grace period, specifically for value chain disclosures. Many data points are subject to phase in, which means that companies can choose to disclose them in subsequent years, while they work on surfacing the data within their business. During the grace period, companies may omit such data and instead disclose their efforts to obtain this information, the reasons for its omission, and plans to obtain the data.

Data collection and management

Understanding regulatory requirements

Double Materiality Assessment

Financial Cost

Senior leadership buy-in

The CSRD seeks to elevate sustainability reporting to the same standard as financial reporting, requiring companies to understand and address risks across their entire value chain. This ambitious and detailed regulation aims to transform the role of sustainability within corporate business models. Novata has identified the following key challenges when it comes to aligning with the CSRD:

01 The Process is Resource- and Cost-Intensive. Based on a double materiality assessment, companies must independently report and verify more than 1,000 data points, covering everything from greenhouse gas emissions to gender pay differences and human rights issues. According to Novata’s recent CSRD survey, over 50% of companies anticipate annual compliance costs to exceed €100,000. Costs are expected to be proportional to organisation size, as larger organisations have more data to collect and assure, as well as more complex value chains to assess for their DMA. Additional factors that may affect implementation costs include the complexity of business models, particularly in high-risk industries that demand specialised expertise for DMA.

02 It Covers Many Layers, Including Value Chain.The CSRD mandates that companies disclose significant ESG impacts, risks, and opportunities (IROs) associated with their entire value chain, both upstream and downstream. This requirement extends beyond evaluating IROs within a company’s direct supply chain and may include impacts on farm workers outside company control or environmental factors linked to raw material production, even when these processes are not directly managed by the company.

To understand and assess these IROs within the value chain, companies will need a more granular view through a value chain mapping exercise, which illustrates how their business impacts different stakeholders at each step of their value creation process. Consequently, companies outside the direct scope of the CSRD may also be affected by data requests from companies subject to CSRD, as they seek to gain a better understanding of IROs. Additionally, companies required to report under the CSRD will need to strengthen communication channels within their value chains to obtain the necessary data and information.